Gambling Losses Capped to Gambling Winnings: The IRS Math Explained (2026)

Gambling losses capped to gambling winnings is the golden rule you must master. Understand the session accounting method, IRS limitations, and how to maximize your tax savings legally in 2026.

Gambling Losses Capped to Gambling Winnings: The Ultimate IRS Math Guide

Attention: You’ve had a rollercoaster year at the sportsbook—huge wins followed by crushing defeats—and now you’re looking at your bankroll, realizing you’ve barely broken even.

Problem: When tax season arrives, you discover the IRS doesn’t care if you “broke even” in your head; they see every win as income and every loss as a hurdle. The most frustrating rule you will encounter is that gambling losses capped to gambling winnings are the maximum relief you can get.

Promise: In this comprehensive guide, we will deconstruct the “Cap Rule,” explain the mathematics of session accounting, and show you how to navigate these IRS limitations so you don’t pay more than your fair share.

IRS Rules 2026: How Uncle Sam Classifies Your Gambling Wins

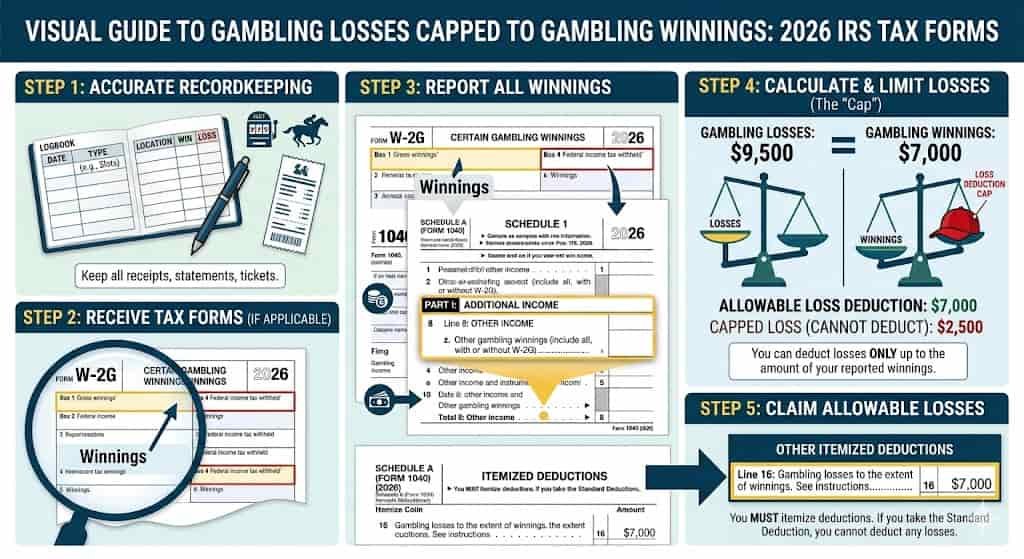

Before understanding the deductions, we must realize that the IRS treats gambling income as “other income.” Whether it’s a $1,000 slot jackpot or a $50 lottery win, it is all taxable. The IRS doesn’t just want to know your net profit at the end of the year; they want to know the “Gross” amount of every win.

This creates a tax liability immediately. For instance, if you win $10,000 but lose $10,000, you technically have $10,000 in income that needs to be reported. This is why the gambling loss deduction is your most important tool. Without it, you would be paying taxes on money you don’t even have in your pocket anymore.

Are Gambling Losses Tax Deductible? Why Itemizing is Your Only Way Out

2")

One of the biggest traps for casual players is the standard deduction. To answer the question, “Are gambling losses tax deductible?“, the answer is a conditional “yes.” You can only claim these losses if you choose to itemize your deductions on Schedule A.

In 2026, the standard deduction is quite high. If your gambling losses, combined with other itemized deductions like mortgage interest or charitable donations, do not exceed the standard deduction, you cannot claim your losses. This means you will pay tax on your winnings but get no benefit from your losses. This is the “tax gap” that catches many unprepared bettors.

The Hard Truth: Why Gambling Losses Capped to Gambling Winnings is the Rule

The core of the IRS policy is that gambling is a hobby, not a business (for most people). Therefore, gambling losses capped to gambling winnings is the absolute limit. You cannot use a loss at the casino to offset your salary or income from your business.

The Mathematics of the Cap

If you have $20,000 in total winnings and $30,000 in total losses, your deduction is capped at $20,000. That remaining $10,000 in losses is “disallowed.” You cannot carry it over to next year, and you cannot use it to lower the taxes you owe on your professional salary. This “dollar-for-dollar” cap ensures the government never loses tax revenue from your gambling activity, even if you are deep in the red.

The “Session Accounting” Hack for Smart Players

3")

Since you are a reader of GamblingHacks.net, you need to know the most effective legal way to lower your gross income: Session Accounting.

The IRS allows you to “net” your results within a single session. A session is generally defined as a continuous period of play on the same type of game at the same location.

- The Wrong Way: Reporting every winning spin and every losing spin separately.

- The Pro Hack: If you play slots for 4 hours, start with $500 and leave with $900, your “Gross Win” for that session is only $400.

By using session accounting, you naturally keep your reported winnings lower, which means you don’t have to worry as much about the “capped” rule affecting your Adjusted Gross Income (AGI).

2026 Updates: New Tax Law Gambling Losses Every Player Should Know

The landscape for 2026 has become much stricter regarding digital tracking. Under the new tax law gambling losses provisions, the IRS is receiving more data than ever from legal sportsbooks and online casinos.

There is now a heavier emphasis on “Session-Based” reporting. If you are audited, the IRS will look for a “contemporaneous” log—meaning a record created at the time of play, not months later. Furthermore, the 2026 updates clarify that “indirect expenses” such as travel, hotel, or betting software subscriptions are not deductible for casual players. Only the “wager” itself counts toward your gambling loss deduction.

Game-Specific Insights: How the Cap Rule Applies to Slots, Poker, and Sports

Not every game is treated the same when it comes to the gambling loss deduction.

- Slots & Video Poker: These are ideal for session accounting. One day at one casino equals one session.

- Poker Tournaments: Each tournament is usually its own session. If you enter three tournaments and win one, you must report the win from the one and the buy-ins from the others as separate line items.

- Sports Betting: Each bet is technically a session unless you are betting on multiple games simultaneously through a single account in a way that the IRS accepts as a “wagering pool.”

Audit-Proof Your Return: How to Prove Your Losses to the IRS with Certainty

If you claim that your gambling losses capped to gambling winnings are a certain amount, the IRS will demand proof. A “feeling” or a bank statement showing a withdrawal isn’t enough. You need:

- The Gambling Diary: A detailed log showing dates, game types, casino names, and win/loss amounts.

- Win/Loss Statements: These are provided by casinos via your player’s card.

- Physical Proof: Keep your losing betting slips, unredeemed lottery tickets, and bank records.

Tax Efficiency Strategy: Legally Maximizing Your Gambling Loss Deduction in 2026

To make the most of your tax situation, follow these “hacks”:

- Avoid Rounding: Reporting exactly $10,000 in wins and $10,000 in losses is a massive red flag. Use exact numbers like $10,142.

- Year-End Timing: If you have a large win in December, consider your losses for that same month. Losses from January 1st of the next year cannot offset your December win.

- Consult a Professional: If your winnings are significant, a tax professional can help you decide if you qualify for “Professional Gambler” status, which changes the rules entirely.

Frequently Asked Questions

Q: Can I carry over my losses to next year?

No. Gambling losses must be used in the same tax year they occurred.

Q: Do I have to report wins if the casino didn’t give me a W-2G?

Yes. All winnings are taxable, regardless of whether a form was issued.

Q: Can my spouse’s losses offset my wins?

If you file a joint return, your combined losses can offset your combined winnings, subject to the same “capped” rule.

4")

Conclusion: The Final Hack

Mastering the math of taxes is just as important as mastering the odds of the game. Understanding that are gambling losses tax deductible only through itemization and that gambling losses capped to gambling winnings is the golden rule will save you from expensive mistakes. Stay disciplined with your record-keeping, and you will always be one step ahead of the IRS.

For more expert advice and the latest iGaming trends, visit GamblingHacks.net.